Price hedging for coffee, using the futures market

DOI:

https://doi.org/10.29312/remexca.v13i6.3313Keywords:

futures market, hedging, risk, utility, volatilityAbstract

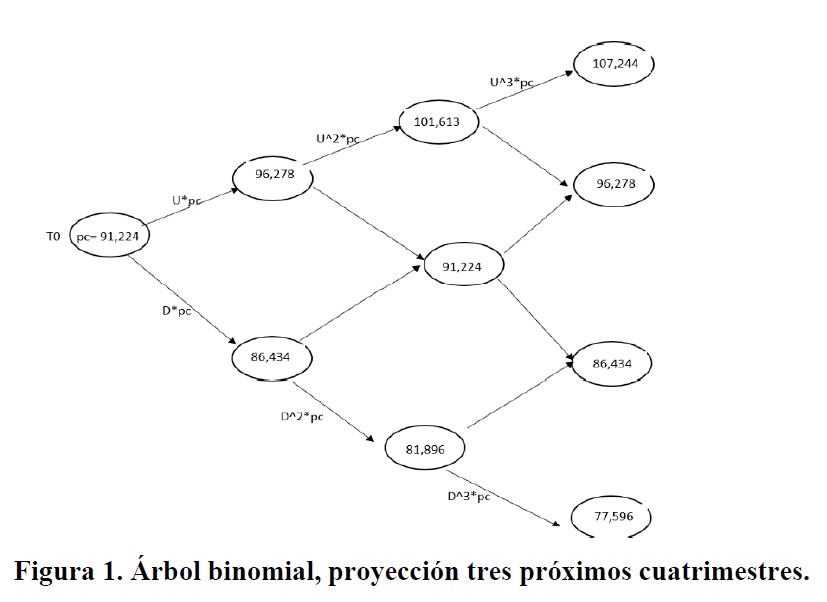

The present work completed in January 2021 determined a price hedging model in the coffee futures markets. Following the analytical method, first, the behavior of the historical prices from January 2015 to December 2020 in the spot market and in the futures market was observed and analyzed, later using the standard deviation of the historical data, the volatility that exists in the futures market and its impact on the final price that producers receive for their harvest at the end of each production cycle was calculated. Applying the statistical theory of the binomial tree, the expected prices of the following three four-month periods are estimated, subsequently, the utility function of the producer is modeled, assuming it as the expectation of income and its variance, later the utility function of the producer is found and optimized to know the number of contracts that guarantees the hedging of the price of production. The results of this work suggest that the final income of the producer will depend directly on the production that is expected to have in each productive cycle, on the speculative game on the stock exchange (number of contracts) and on the forecast of the spot price at the time of the evaluation, finally, it is concluded that the producers could be motivated to use futures contracts as a hedging strategy, since even if the profits are not extraordinary, the income will always be higher when such hedging is used.

Downloads

References

Black, F. and Scholes, M. 1973.The pricing of options and corporate liabilities. EE. UU. J. Pol. Econ. 3(81):637-654. DOI: https://doi.org/10.1086/260062

Cárcamo, U. C. 2008. Modelos de tiempo continuo para commodities agrícolas en Colombia. Colombia. Ad-minister. 11(1):42-63.

CEDRSSA. 2018. Centro de estudios para el desarrollo rural sustentable y la soberanía alimentaria. El café en México. obtenido de: http://www.cedrssa.gob.mx.

FIRA. 2011. Fideicomisos Instituidos en Relación con la Agricultura. Mercado de futuros y Opciones. México. FIRA Boletín. 11(1):6-7.

García, V. V. M. y Porras, A. 2009. Modelos Estocasticos para el Precio Spot y del Futuro de Commodities con alta volatilidad y reversión a la media, México. Revista de Administración, Finanzas y Economía. 2(3):1-24.

Gutiérrez, R. 2018. Predicción de las razones de cobertura cruzada optima en el mercado del petróleo mexicano. México. Revista Mexicana de Economía y Finanzas Nueva Época. REMEF. 1(13):48-67. DOI: https://doi.org/10.21919/remef.v13i1.259

Hull, J. C. 2011. Introducción a los mercados de futuros y opciones. México: Pearson educación.

Mariz, N. A. 2016. Modelización estocástica de acciones mediante arboles binomiales. España. Rev. Leopoldo Pons.

Merton, C. R. 1973.Theory of rational option pricing. EE.UU. The bell journal of economics and management science.1(4):141-183. DOI: https://doi.org/10.2307/3003143

Investing. 2020. Investing.com. https://mx.investing.com/commodities/us-coffee-c-historical-data.

Ochoa, C. M. 2009. Metodologías alternativas para la valoración de opciones americanas sobre TRM. Repositorio Institucional EAFIT.

Ramírez, F. O. 2006. Modelación de la volatilidad y pronóstico del precio del café. Colombia. Rev. Ingenierías Universidad de Medellín. 9(5):45-58.

Solares, D. O. 2011. Contrato C, principales características. Guatemala.

Working, H. X. 1953. Futures traiding and hedging. EE. UU. American economic review. 3(43):314-343. http://www.ico.org/es/new-historical-c.asp.

Published

How to Cite

Issue

Section

License

Copyright (c) 2022 Revista Mexicana de Ciencias Agrícolas

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

The authors who publish in Revista Mexicana de Ciencias Agrícolas accept the following conditions:

In accordance with copyright laws, Revista Mexicana de Ciencias Agrícolas recognizes and respects the authors’ moral right and ownership of property rights which will be transferred to the journal for dissemination in open access. Invariably, all the authors have to sign a letter of transfer of property rights and of originality of the article to Instituto Nacional de Investigaciones Forestales, Agrícolas y Pecuarias (INIFAP) [National Institute of Forestry, Agricultural and Livestock Research]. The author(s) must pay a fee for the reception of articles before proceeding to editorial review.

All the texts published by Revista Mexicana de Ciencias Agrícolas —with no exception— are distributed under a Creative Commons License Attribution-NonCommercial 4.0 International (CC BY-NC 4.0), which allows third parties to use the publication as long as the work’s authorship and its first publication in this journal are mentioned.

The author(s) can enter into independent and additional contractual agreements for the nonexclusive distribution of the version of the article published in Revista Mexicana de Ciencias Agrícolas (for example include it into an institutional repository or publish it in a book) as long as it is clearly and explicitly indicated that the work was published for the first time in Revista Mexicana de Ciencias Agrícolas.

For all the above, the authors shall send the Letter-transfer of Property Rights for the first publication duly filled in and signed by the author(s). This form must be sent as a PDF file to: revista_atm@yahoo.com.mx; cienciasagricola@inifap.gob.mx; remexca2017@gmail.

This work is licensed under a Creative Commons Attribution-Noncommercial 4.0 International license.